How to save money: proven budgeting strategies that work

- teamlifesowell

- Apr 23

- 10 min read

TL;DR:

Budgeting reduces stress and enhances financial control by showing where money goes.

Effective savings habits include automation and small daily routines like meal prepping and subscription audits.

Flexibility and self-compassion are vital for lasting financial progress and emotional wellbeing.

Money stress has a way of creeping into everything, from your sleep to your relationships. You know you should be saving, but between rent, groceries, subscriptions, and the occasional emergency, there never seems to be enough left over. The good news is that saving money is less about willpower and more about having the right system. When you combine a clear budget with a few smart habits, you stop reacting to your finances and start leading them. This guide walks you through practical, proven strategies to budget well, save consistently, and ease the emotional weight that money problems tend to carry.

Table of Contents

Understanding why saving feels hard—and how budgeting changes everything

Choosing the right budgeting method: 50/30/20, zero-based, or hybrid?

Automate, optimize, and stick with it: Habits for saving money that last

Troubleshooting and tips: Tackling common roadblocks and staying on track

Our take: Why flexibility and self-compassion matter most for lasting savings

Key Takeaways

Point | Details |

Budgeting boosts savings | Using a written budget can help you save thousands more each year. |

Pick a method that fits | Choose a budgeting style, like 50/30/20 or zero-based, that matches your lifestyle and income. |

Make saving automatic | Automate transfers or pay yourself first to make saving effortless. |

Review and adjust | Check your budget monthly to spot issues, celebrate wins, and keep improving. |

Understanding why saving feels hard—and how budgeting changes everything

Most people do not struggle to save because they are careless. They struggle because no one ever taught them how. Financial education is rarely a priority in school, and by the time adulthood hits, the bills are already stacking up. Add in lifestyle inflation, where your spending quietly expands as your income grows, and you have a cycle that is genuinely hard to break.

There is also an emotional layer that gets underestimated. When money feels tight, stress and anxiety take over, and those feelings actually make it harder to think clearly and take action. It becomes a vicious cycle: financial pressure triggers emotional overwhelm, which blocks the focused thinking you need to solve the problem. This connection between money stress and mental wellbeing is real, and it is why wellness and mental health practices often overlap with financial advice.

Here is where budgeting becomes a genuine game-changer. A budget is not a punishment. It is a map. It shows you exactly where your money is going so you can make intentional decisions rather than guessing. Research shows that budgeting reduces stress and boosts financial control, with a significant share of budgeters reporting they feel more in charge of their financial lives.

Think of a budget like a thermostat. Without one, your finances swing between too hot and too cold with no predictability. With one, you set a target and your spending stays within range.

Common barriers that keep people from budgeting include:

Unexpected expenses that seem to blow up any plan you make

Lifestyle inflation that silently absorbs every raise or bonus

Lack of a starting point, which makes the whole thing feel too overwhelming

Emotional avoidance, where looking at your finances feels worse than ignoring them

Perfectionism, where the fear of doing it wrong stops you from starting at all

“A budget is telling your money where to go instead of wondering where it went.” This simple shift in mindset is what separates people who feel financially stuck from those who feel financially free.

Once you understand the barriers, you can address them directly, and that is exactly what the rest of this guide will help you do.

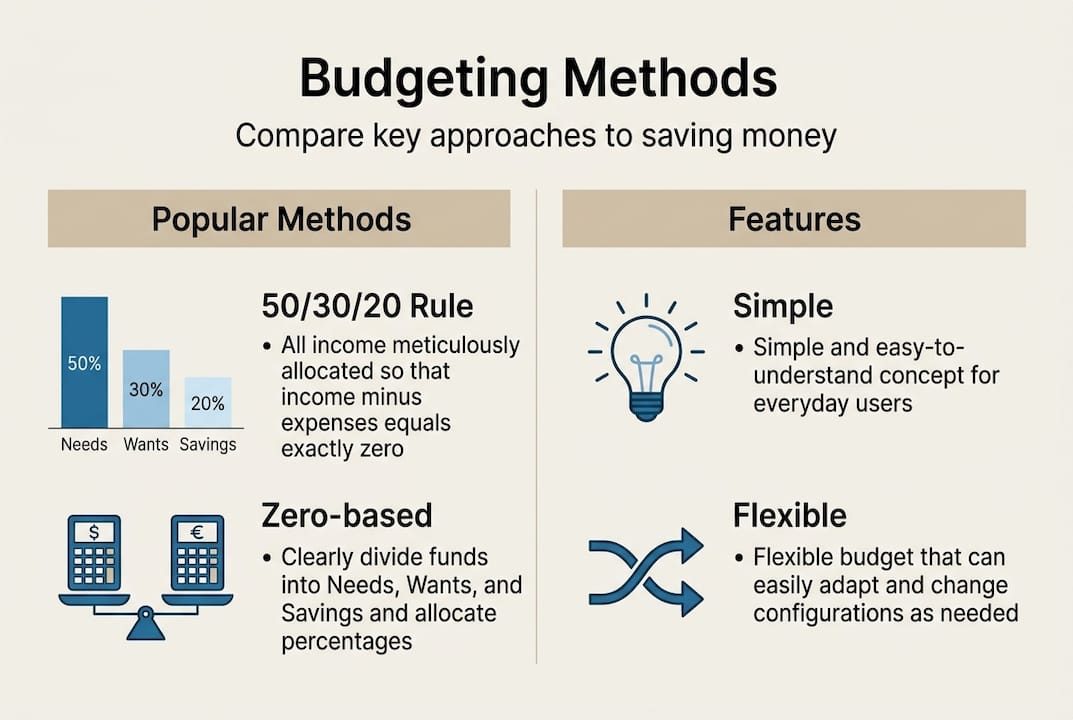

Choosing the right budgeting method: 50/30/20, zero-based, or hybrid?

There is no single budgeting method that works for everyone. Your income type, lifestyle, and financial goals all play a role in which approach will actually stick. The key is to start with a framework, then adapt it to fit your real life.

The 50/30/20 rule is one of the most popular starting points because it is simple and flexible. You divide your after-tax income into three buckets: 50% for needs (housing, food, utilities, transportation), 30% for wants (dining out, entertainment, hobbies), and 20% for savings and debt repayment. It is a clean structure that works well for most salaried workers. However, the 50/30/20 rule needs adjusting if you live in a high-cost city or have irregular income, since fixed costs alone may eat up more than half your paycheck.

Zero-based budgeting takes a more disciplined approach. Every dollar you earn is assigned a job, whether that is rent, groceries, an emergency fund, or entertainment. At the end of the month, your income minus your expenses equals exactly zero. Nothing is left unaccounted for. Zero-based budgeting gives more control, especially for people focused on paying off debt, because it forces intentionality with every spending decision.

Hybrid methods blend the structure of these two approaches with built-in flexibility. They are especially useful for freelancers or anyone with variable income, since you can base your budget on a conservative income estimate and adjust each month as actual earnings come in.

Method | Best for | Effort level | Flexibility |

50/30/20 | Steady income, beginners | Low | High |

Zero-based | Debt payoff, detail-oriented | High | Low |

Hybrid | Variable income, mixed goals | Medium | Medium |

Pro Tip: If budgeting is new to you, start with the 50/30/20 rule. It is forgiving enough to learn from and structured enough to create real change. Once your habits are solid, you can explore the best budgeting apps to automate and refine your process.

Set up your budget: Tools, steps, and a real-world example

Knowing which method to use is step one. Actually building your budget is where the real transformation begins. The good news is that setting up a budget does not require a finance degree or a fancy tool.

You can use a dedicated app, a spreadsheet, or even a notebook. Digital tools sync with your bank, categorize spending automatically, and send alerts when you overspend. Spreadsheets offer full customization without a subscription fee. Paper budgets work well for visual learners who want a tactile experience. The right tool is simply the one you will open and use every week.

Here are the steps to build your first budget:

Gather your financial information. Collect your last two to three pay stubs, your monthly bills, and three months of bank or credit card statements.

Track your spending. Look at what you actually spent last month, not what you think you spent. Most people are surprised.

Categorize your expenses. Group them into needs, wants, and savings or debt repayment.

Set spending limits for each category. Use your chosen method (50/30/20, zero-based, or hybrid) as your guide.

Review after the first month. Your first budget will not be perfect, and that is expected. Adjust based on real patterns.

Here is a sample monthly budget for a take-home income of $3,500:

Category | Allocation | Monthly amount |

Housing | 30% | $1,050 |

Food and groceries | 12% | $420 |

Transportation | 8% | $280 |

Utilities and bills | 7% | $245 |

Wants and fun | 23% | $805 |

Savings and emergency fund | 20% | $700 |

Households that commit to written budgets save $6,300 more per year on average. That is a meaningful ripple effect from one habit. Pairing your budget with supportive daily routines, like those found in a solid wellness habits workflow, can make the whole practice feel more sustainable.

Pro Tip: After your first month, flag the categories where you overspent and ask why. Was it a one-time event, or is your target unrealistic? Adjusting early makes the habit stick.

Automate, optimize, and stick with it: Habits for saving money that last

A budget on paper is just a plan. Turning it into results requires habits that do the work for you, even on your busiest or most stressed-out days.

Automation is the single most powerful tool in your savings toolkit. When you set up an automatic transfer from your checking account to your savings account on payday, you never have a chance to spend that money. It disappears before you see it, and you adjust your lifestyle around what remains. People who automate their savings save an average of 23% of their take-home pay, compared to a median of 15% among those who save manually.

Beyond automation, small everyday habits create a surprising domino effect:

Pack lunch three days a week. At $10 to $15 per meal out, that adds up to $150 or more each month.

Audit your subscriptions every quarter. Most people are paying for at least one service they forgot about.

Try the 52-week savings challenge. Save $1 in week one, $2 in week two, and so on. By year’s end, you have saved $1,378.

Use the 24-hour rule before any non-essential purchase over $50. Most impulse urges fade within a day.

Celebrate small wins. Saved your first $500 emergency fund? Acknowledge it. Positive reinforcement is a real motivator.

For ideas on building a habits workflow for progress that connects financial and personal growth, there are practical frameworks worth exploring. And if you want a broader look at strategies, the more money tips section on Life So Well covers a wide range of financial wellness topics.

Pro Tip: Schedule a 15-minute budget check-in on the same day every month. Treat it like an appointment. Consistency here is what separates short-term motivation from lasting change.

Troubleshooting and tips: Tackling common roadblocks and staying on track

Even with the best intentions and a solid plan, there will be months where something goes sideways. A car repair shows up, a medical bill lands, or you simply overspend on a vacation. This is normal. What matters is how you respond.

The most common mistake people make after a slip-up is quitting entirely. One bad month does not erase the progress you made. Progress is always more important than perfection, and treating a setback as feedback rather than failure keeps you moving forward.

Here are some practical ways to handle the most common obstacles:

Unexpected expenses: Build a dedicated emergency fund with at least one month of expenses before you aggressively grow other savings. This buffer absorbs shocks without destroying your budget.

Motivation dips: Revisit your “why.” Write down what you are saving toward and put it somewhere visible. A concrete goal (a home, a trip, debt freedom) is a far stronger motivator than a vague sense of being responsible.

Peer pressure: Social spending is a real challenge. Practice saying “I am working toward a goal right now” rather than deflecting with excuses. Most people respect honesty.

Budget fatigue: Simplify. If your system feels like too much work, strip it down to three categories and rebuild from there.

Tracking your progress visually, whether through a savings chart, a milestone list, or even a simple spreadsheet graph, creates a feedback loop that reinforces new behavior. Consistent self-care routines for wellness also play a surprising role here, since managing stress through sleep, movement, and mindfulness makes it easier to stay consistent with any goal, financial or otherwise.

“Budgeters are 2.5 times more likely to be financially healthy than non-budgeters.” That gap is not about income. It is about intention and a system that creates it.

Budgeting is not a one-time project. It is an ongoing conversation with yourself about what matters, what does not, and how you want to live.

Our take: Why flexibility and self-compassion matter most for lasting savings

Here is something that most financial advice misses: rigid systems often backfire. When a budget is too strict, even one slip creates a spiral of guilt that makes people abandon the whole thing. We have seen this pattern repeatedly, and it is one of the most frustrating ways people lose progress they worked hard to build.

The most successful savers are not the ones with the most detailed spreadsheets. They are the ones who forgive themselves quickly and adjust without drama. Flexibility is not weakness. It is what makes a financial plan durable enough to survive real life.

We also believe that emotional wellness and financial wellness are deeply connected. When you feel calmer and more grounded, you make better money decisions. That is why exploring wellness habits and finances together is not a detour from your savings goal. It is actually a shortcut. Your system does not need to be perfect. It needs to be yours.

Ready to take control of your finances?

Building a savings habit is one of the most powerful things you can do for your wellbeing, and you do not have to figure it out alone. Life So Well offers a growing library of resources designed to support your financial health alongside your emotional resilience.

Whether you are navigating financial stress support or looking for practical ideas in our money wellness resources hub, there is something here for wherever you are in your journey. Explore, bookmark what resonates, and take your next step with confidence. Real progress starts with one honest look at your finances and one small action that follows.

Frequently asked questions

What is the easiest way to start saving money if I’ve never budgeted before?

Start by tracking all your expenses for one month, then use the 50/30/20 rule to divide your income into needs, wants, and savings. It is beginner-friendly and gives you immediate clarity without overwhelming detail.

Are budgeting apps better than spreadsheets or paper?

Apps automate tracking and flag overspending in real time, but the best budget method is the one you will actually use week after week. Try one approach for 30 days before deciding it works or does not.

How much should I save each month?

The 50/30/20 rule recommends setting aside 20% of your income for savings and debt repayment. If that is not realistic right now, start with 5% and increase it gradually as you free up spending in other areas.

What if my expenses are too high to save anything?

Focus first on cutting one discretionary category and redirect that amount to automated savings. Even $25 a month builds momentum and the habit of saving, which matters as much as the dollar amount in the early stages.

Recommended

Comments